Top Five Technology Trends Driving Wealth Management

In recent years, technological innovations have significantly transformed the landscape of asset and wealth management (AWM). These advancements have enabled wealth managers to develop more sophisticated strategies and played a pivotal role in shaping the industry’s evolution. In this blog, let’s see what the CTOs of leading global AWM companies have to say about the top five technology trends driving wealth management’s future and how these trends are reshaping the industry’s landscape.

Wealth Management Solutions

Partnering with AWM Technology consulting firms like Maveric, with deep domain knowledge, is an effective way to create competitive differentiation. It also underscores that technology offers a powerful strategy to navigate the frequently changing industry landscape.

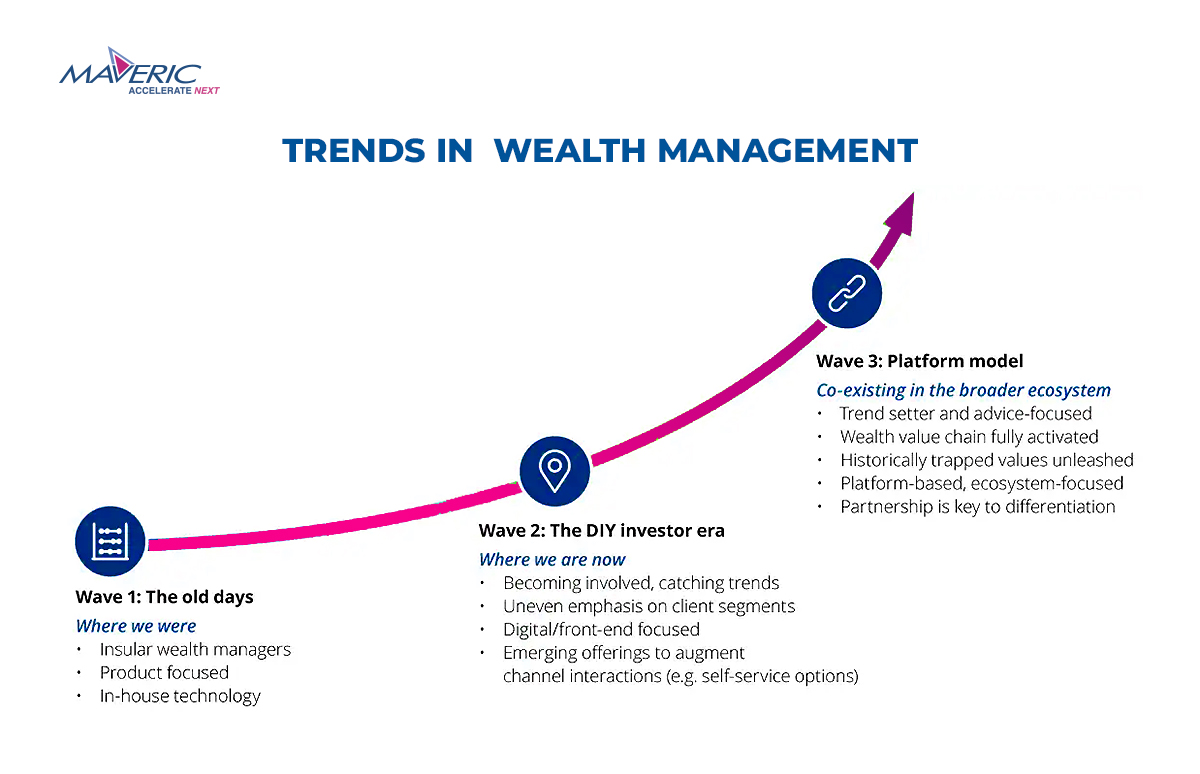

Evolution of Asset and Wealth Management and Technological Advancements

The world of AWM has experienced a remarkable evolution, driven by changing demographics, generational wealth transfer, and the rapid expansion of digitalization. Customers now demand a broader array of investment options and a seamless service experience, while relationship managers are empowered by real-time data access and digital tools. Technology has emerged as a transformative force, underpinning the industry’s growth and customer-centric approach.

Trend 1: Integration of AI, ML, and Automation for Digital Wealth Management

Emergent techs like AI and ML have taken center stage in wealth management, revolutionizing portfolio management, risk assessment, and investment decision-making. By analyzing vast volumes of data and identifying intricate patterns, AI and ML provide wealth managers with accurate predictions and insights, enabling informed decisions. Furthermore, Robotic Process Automation (RPA) automates routine tasks, helping precious human resources go after more strategic responsibilities. Deloitte predicts that by 2025, Robo-Advisors will manage $16 trillion in assets under management (AUM).

Trend 2: Robo-Advisory Revolution in digital wealth management platform

Robo-advisory is a pivotal trend shaping the future of wealth management. These software platforms analyze investment trends and opportunities based on individual investor profiles, risk tolerance, and goals. Using AI and advanced ML technologies empowers wealth managers to create tailored investment portfolios effortlessly. As a testament to this trend, Capgemini’s World Wealth Report indicates that 55% of High-Net-Worth Individuals (HNWIs) invest in causes with positive Environmental, Social, and Governance (ESG) impacts.

Trend 3: Digital Wealth Platforms

The emergence of digital wealth platforms signifies a paradigm shift in portfolio management and client engagement. These platforms leverage Machine Learning algorithms to analyze market data and provide sophisticated financial decisions, enabling investors to make informed choices without human intervention. The agility and automation offered by digital wealth platforms enhance portfolio management, client onboarding, and reporting, reducing risks and higher returns.

Trend 4: Harnessing Big Data Analytics and Alternative Data Sources

The proliferation of data sources and alternative data has opened new avenues for investment managers. Big Data analytics enables wealth managers to gain unique insights, identify investment opportunities, and manage risk more effectively. The data-driven approach redefines decision-making processes and offers an industry competitive edge.

Trend 5: Embracing ESG as an Investment Strategy for Wealth Management Services

Environmental, Social, and Governance (ESG) considerations reshape the investment landscape. Investors increasingly integrate ESG criteria into their portfolios, seeking sustainable and socially responsible investments. Wealth managers adapt to this trend by incorporating ESG principles into their investment strategies, meeting market demand for ethical and sustainable options.

GPT AI and the Future of Digital Wealth Management Platforms

As the technology landscape evolves, the influence of AI is poised to expand further, with innovations like GPT AI beginning to make their mark in the AWM sector. GPT AI’s ability to analyze vast amounts of data and generate human-like text transforms how wealth managers interact with clients, automate customer communications, and provide personalized insights. The integration of GPT AI can enhance customer engagement, streamline communication, and improve the wealth management experience.

The Road Ahead: Key Considerations for CTOs and CIOs

In this dynamic landscape, CTOs and CIOs of wealth management firms must consider several pivotal questions:

- How can we harness AI and ML to enhance investment strategies and client engagement?

- How can we ensure seamless integration of robo-advisory platforms and digital wealth solutions?

- How can we leverage big data analytics to uncover unique investment insights and manage risk?

- What strategies should be implemented to incorporate ESG principles and meet the growing demand for sustainable investments?

- How can we strategically adopt GPT AI to enhance client interactions and automate communication processes?

Conclusion

By addressing these questions and embracing these technology trends, wealth management firms can position themselves for sustainable growth, operational efficiency, and continued success in the ever-evolving AWM landscape.

About Maveric Systems

Starting in 2000, Maveric Systems is a niche, domain-led Banking Tech specialist partnering with global banks to solve business challenges through emerging technology. 3000+ tech experts use proven frameworks to empower our customers to navigate a rapidly changing environment, enabling sharper definitions of their goals and measures to achieve them.

Across retail, corporate & wealth management, Maveric accelerates digital transformation through native banking domain expertise, a customer-intimacy-led delivery model, and a vibrant leadership supported by a culture of ownership.

With centers of excellence for Data, Digital, Core Banking, and Quality Engineering, Maveric teams work in 15 countries with regional delivery capabilities in Bangalore, Chennai, Dubai, London, Poland, Riyadh, and Singapore. Contact Maveric Systems today!

View