The Role of CFOs In Driving ESG Transformation

As ESG (Environmental, Social, and Governance) metrics evolve into critical components of financial strategy, the responsibility for managing ESG data is shifting toward CFOs and finance teams. This transition is driven by the financialization of ESG data, where sustainability metrics are increasingly linked to financial performance and regulatory compliance. Given the rising investor expectations and stricter regulatory demands, CFOs in asset management firms are uniquely positioned to lead ESG governance, enhance data quality, and ensure that ESG initiatives align with the organization’s financial objectives.

Traditionally managed by risk and compliance teams, ESG data now falls under the purview of finance, reflecting its growing importance to shareholder value. This blog explores the expanding role of CFOs in ESG transformation, detailing how asset managers can establish a collaborative governance model between finance and compliance, optimize data management, and prepare for long-term sustainable growth.

The Shift in ESG Data Ownership: From Compliance to Finance

Historically, due to its regulatory and reputational implications, ESG data has been the domain of risk and compliance teams. However, as ESG metrics become financially relevant, asset managers are adopting a more collaborative approach involving finance and compliance teams in managing ESG data. This shift creates a more cohesive governance model, positioning finance as a key player in driving ESG integration and aligning sustainability initiatives with the firm’s financial objectives.

To meet these complex requirements, asset managers should consider a CFO-led governance structure that centralizes ESG oversight, leverages advanced technology for data quality, and enhances the financial integration of ESG data. This evolving approach to ESG ownership is outlined below, comparing current and recommended practices to illustrate how the collaborative model strengthens ESG governance and reporting.

‘This may vary across asset managers, however, this is a generalized ownership model.’

‘This may vary across asset managers, however, this is a generalized ownership model.’

By adopting this structured, CFO-led model, asset managers can achieve a cohesive and integrated approach to ESG data governance, ensuring compliance and financial integration are aligned with global and regional ESG standards.

Key Responsibilities of CFOs in Leading ESG Transformation

As ESG becomes a core component of financial performance, CFOs in asset management are tasked with integrating ESG metrics into financial reporting, enhancing data quality, and driving strategic alignment with long-term goals. The following key responsibilities help finance teams support and lead ESG initiatives effectively:

1) Establishing Centralized Governance and Accountability

As ESG data becomes financially material, centralizing ESG governance under the CFO ensures that sustainability metrics are held to the same standards as financial data. This centralized model allows CFOs to create consistent data practices, enhance transparency, and promote accountability across the organization.

Benefit for Asset Managers:

With a CFO-led framework, ESG initiatives align with financial strategies, creating a cohesive view of the firm’s financial and non-financial risks and enhancing decision-making capabilities.

2) Implementing Robust Data Management and Validation Processes

ESG data must be reliable, accurate, and rigorously validated to meet regulatory standards. As leaders in ESG data management, CFOs are responsible for deploying RegTech tools that automate data collection and validation, ensuring high data quality and minimized operational inefficiencies.

Enhanced Data Assurance:

Technologies such as EcoVadis or Workiva enable automated data checks and validation, significantly reducing manual touchpoints. This automation supports asset managers’ compliance with region-specific requirements, such as the EU’s CSRD, which mandates double materiality and third-party assurance.

3) Integrating ESG Metrics into Financial Reporting

As ESG data becomes financially relevant, CFOs must translate it into insights directly impacting portfolio decisions and shareholder value. Integrating ESG metrics with financial data allows asset managers to evaluate sustainability risks and opportunities across their portfolios, helping them make informed investment choices aligned with long-term objectives.

Driving Long-Term Value:

By embedding ESG metrics in financial reporting, CFOs enable asset managers to quantify the financial impacts of sustainability initiatives, aligning portfolios with investor demands for transparency and accountability.

Conclusion: A Strategic Role for CFOs in ESG Transformation

As asset managers face increasing regulatory scrutiny and investor expectations for sustainability, CFOs play a crucial role in integrating ESG into financial frameworks. By establishing centralized governance, implementing rigorous data management practices, and embedding ESG in financial reporting, CFOs drive compliance and strategic alignment.

This CFO-led approach ensures adherence to ESG standards and strengthens financial performance by aligning sustainability initiatives with long-term investment objectives. However, this transformation is not without cost. Our next blog, will explore “The Cost of ESG Transformation: A Strategic Investment for Long-Term Shareholder Value.”

Stay tuned as we delve into the upfront costs and long-term benefits of ESG initiatives, examining how asset managers can strategically position themselves for sustainable growth and enhanced shareholder value.

Co-authored by Deepak Bhatter, and Venkatesh Padmanabhachari

Maveric’s thought leadership series – E.D.G.E (Experiences Delivered by Global Experts) – handpicks the game-changing technology ideas and pressing functional questions financial institutions must solve today.

These features – reports, whitepapers, podcasts, flyers, blogs, and infographics – are for Banking leaders and Technology evangelists to apply profound trends, the latest opinions, and transformational analyses to boost the performance of their organizations.

About Maveric Systems

Established in 2000, Maveric Systems is a niche, domain-led, BankTech specialist, transforming retail, corporate, and wealth management digital ecosystems. Our 2600+ specialists use proven solutions and frameworks to address formidable CXO challenges across regulatory compliance, customer experience, wealth management and CloudDevSecOps.

Our services and competencies across data, digital, core banking and quality engineering helps global and regional banking leaders as well as Fintechs solve next-gen business challenges through emerging technology. Our global presence spans across 3 continents with regional delivery capabilities in Amsterdam, Bengaluru, Chennai, Dallas, Dubai, London, New Jersey, Pune, Riyadh, Singapore and Warsaw. Our inherent banking domain expertise, a customer-intimacy-led delivery model, and differentiated talent with layered competency – deep domain and tech leadership, supported by a culture of ownership, energy, and commitment to customer success, make us the technology partner of choice for our customers

View

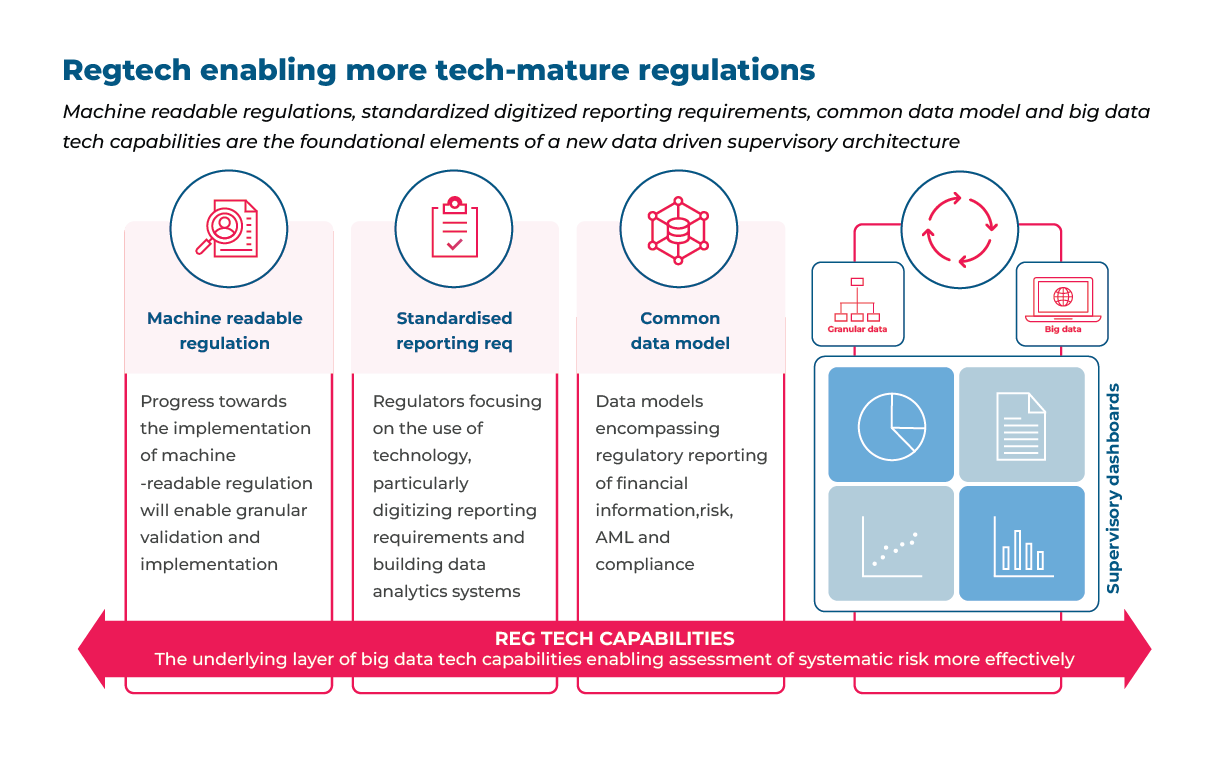

Building a standard data model and standardized reporting requirements is a pre-condition for regulators to ensure they have reliable and comparable data for adequate financial supervision. For the regulatory objectives to be completed, it means that the coverage of CDM and initiatives like digital regulatory reporting is expanded to the majority of reporting entities and, therefore, be built on open standards and is technologically neutral. The technology and methodology must also be scalable across additional reporting domains to be viable.

Building a standard data model and standardized reporting requirements is a pre-condition for regulators to ensure they have reliable and comparable data for adequate financial supervision. For the regulatory objectives to be completed, it means that the coverage of CDM and initiatives like digital regulatory reporting is expanded to the majority of reporting entities and, therefore, be built on open standards and is technologically neutral. The technology and methodology must also be scalable across additional reporting domains to be viable.

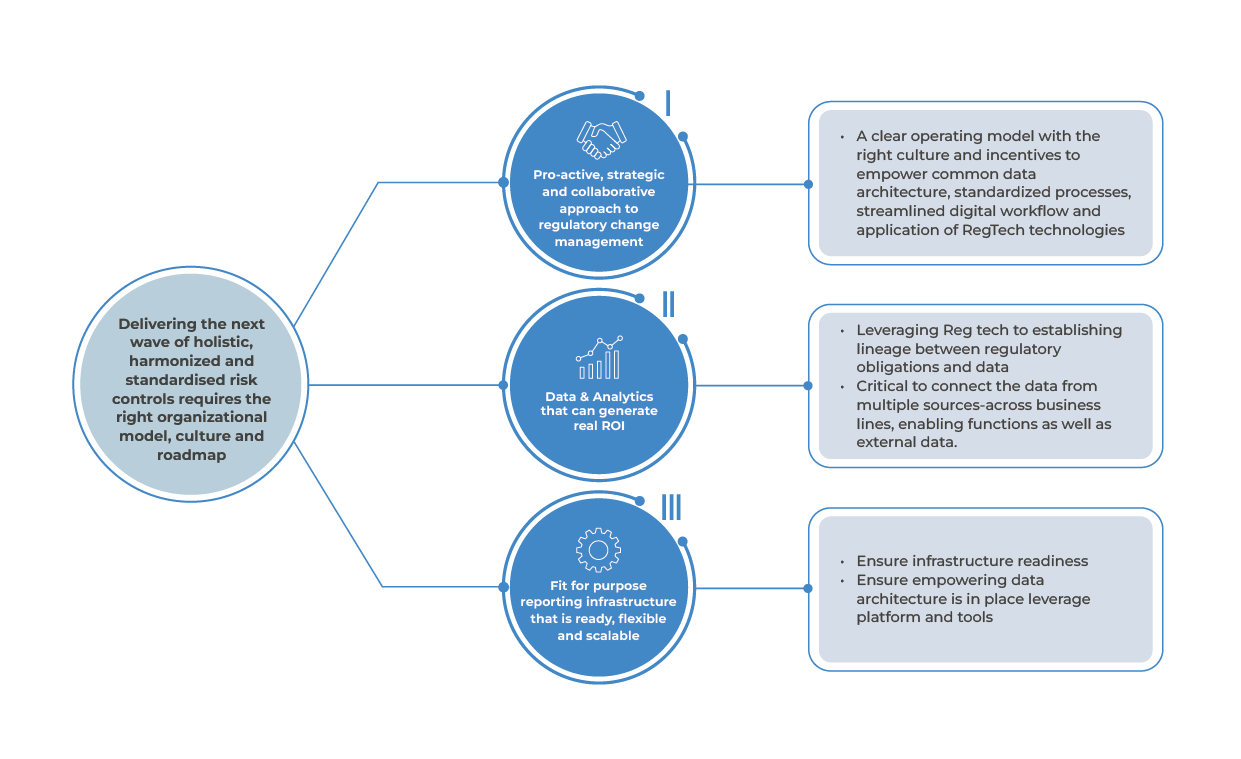

Ensure infrastructure readiness

Ensure infrastructure readiness