A Data Readiness Manifesto in the times of COVID

In a world distanced socially, it appears our work focus has intensified further. With fewer interruptions and the universality of video-collaboration applications, for millions, the nature of work itself is metamorphosing. And so is doing business.

Across geographies and industries, the mounting importance of going digital was never in doubt. But it is now heightened by our changing behaviors forced by COVID.

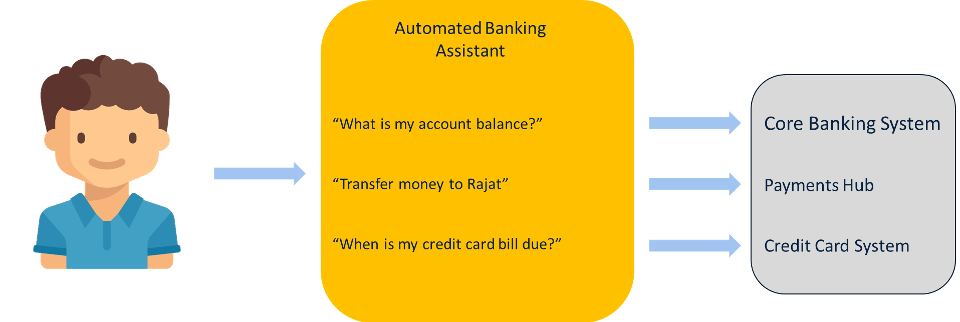

The pandemic is on a path to radically alter ways consumers interact with their businesses. For instance, a May 2020 BCG banking industry report points out that one in four customers is planning to use branchless banking or stop visiting branches altogether after the crisis.

Returning to the beginning of this piece; I realized last month that staring at my laptop for long(er) hours is a pain in the neck. Literally. A pain in my neck. After an exhaustive hypothesis-elimination-exercise, the culprit surfaced: My laptop via its various inadequacies was causing the pain (and the watering eyes).

So in earnest began my shopping expedition for a desktop monitor.

In the COVID period, I quickly found out my favorite computer peripherals store(s) are either locked-down or are barely functional. My trusted product advisors were missing. And gone too was a ‘large swathe of decision-making-wealth’: the fact-finding, needs-analysis, product recommendations, and sales discounts.

For the customer in me, all this counted as an experiential loss. After all, a buyer’s trust-bond is created over many happy hours of exchanging insights and trends.

Questions for digital enterprises (including ones that are planning to go online):

- Is your business recreating a similar customer experience dynamic?

- Does your business listen and engage with your virtual buyers as well as the brick-mortar world?

- Sure you are industriously and enthusiastically posting across a host of social media, but are you able to listen to the customer, probe his needs, zero-in on a buyer’s pain points, perceive buying behavior and demographic preferences, layout product nuances, detail the price comparators, and numerous other variables that close sales?

If my virtual purchase adventure described further is anything to go by, I am guessing answers to the above is negative.

Therein lies the first differentiator (and challenge) precipitated by the COVID times: ‘the human-buying-experience’ has to be replicated (and possibly enhanced) digitally.

The neck pain unrelenting, I took my search online, little knowing that a secondary data-avalanche waited ahead.

Tamr, the data mastering company, in its 2020 survey on the state of data and digital transformation, surveyed 300 C-suite executives in the US financial institutions with revenue of $1 Billion or greater. Here are the key findings,

- Only one percent of those surveyed, are not pursuing digital transformation

- 47 percent say the main drivers of digital transformation is keeping up to the competition.

- 63 percent say data management is a drag on their transformation efforts (because data is unreliable, disorganized, or unusable)

- One in four are dissatisfied with their current methods for managing data velocity, volume, and variety

- 75 percent can’t keep up with constant changes in data over time

- 55 percent say non-scalable data management practices are causing choke-by-data.

- One in two cites ‘speed to insight’ and ‘unifying data across enterprise’ as their primary weakness

- More than fifty percent say they aren’t utilizing their current data to its full potential because it is siloed throughout the organization.

The derived macro-picture is clear in its summary:

Managing data has notable systemic impediments; Inadequate data readiness brings significant drag to digital transformation efforts and finally, there is a strong need for solutions to data volume, variety and velocity.

I called up a few trusted and knowledgeable friends. Soon after, I started with the organization whose name is now a global ‘verb’: Google.

I feed in the phrases and search. And dozens of websites tuned to the latest SEO algorithms show up on my screen immediately.

I proceed to spend much knowledge filled hours on the sites of global (and national) e-retailers. I try the filters: Brand, display size, display technology, monitor resolution types, horizontal and vertical monitor resolution, energy consumption certifications, and average customer reviews. I compare and contrast, I analyze and assimilate, I deduce and deliberate.

Slowly and surely, I learn more and more about anything remotely connected to a computer monitor.

Next, I turn to various product blogs and their expert recommendations: Nifty pictures, neat summaries of features- advantages- benefits and yet, more information. I wade in deeper – refresh rates, response times, aspect and contrast ratios, panel technology, bezel design, curved or flat screen, built-in webcam and speakers, viewing angle, and factor in variables that are unique to my condition – the monitor stand adjustments (height, tilt, swivel, pivot and their permutations thereof).

Needless to say, all facts and information are calibrated against my budget.

All things considered, am I close to make a decision? Not yet.

I find myself asking:

Saved-by-data or death-by-data?

In the absence of a trusted sales professional who listens, diagnoses my need to offer a slew of recommendations, how does a buyer himself join the dots?

Especially for products that lie outside of his area of expertise.

Questions for digital enterprises (including ones that are planning to go online):

- Does your data readiness strategy actively engage the virtual buyer (are their feedbacks and observations collated and correlated)?

- Are your products and services data consistent, well-structured, and in a readable format and aligned to industry aggregators and search engines?

- Does your data enable real-time integration with other sources for analysis?

- Can the data be accessed in repeatable, automatic methods?

- Can the data be tied back to physical sources involved in the production?

- Does your organization have resources to institutionalize knowledge that comes out of data relationships and real-time models?

As ‘data’ continues to systemically restructure our society, our economy, and our institutions in ways unseen since the industrial revolution two and a half centuries earlier, businesses have to accept that data lies at the structural sweet spot between technology, process, and people.

Before enterprises commit to digital investments, they have to consider the various aspects of data governance, namely, integrity, security, availability, and usability.

And even before that, digital (or soon to be) enterprises have to honestly ‘see’ their data readiness.

Just like a holistically deliberated and a uniquely picked monitor is critical to see your work (and keep your health)

This was originally published on www.emergingpayments.org website and is being reproduced here.

View