For decades, financial institutions were seen as places where customers queued, and the inefficient processes caused frustrating delays. In the face of legacy mindsets and compliance mandates, banks, on their part, were hesitant to upgrade their systems.

But most of that is past, as financial institutions face competition from tech-based Fintechs that are nimble and flexible.

The pandemic hastened the incorporation of technology as customer adoption of digital soared as never before. Consider a developmental metric attributable to the pandemic.

The Reserve Bank of India’s (RBI) Annual report shows that the total volume of digital transactions in 2020-21 stood at 4,371 crores, up from 3,412 crores in 2019-20.

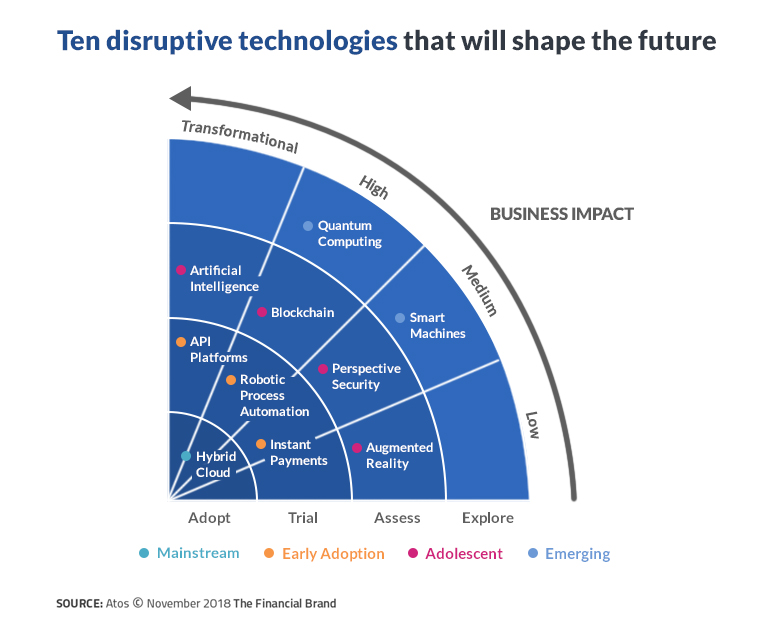

The emergent technologies (think AI, ML, AR, MR, VR, and Quantum Computing) are ushering in a dramatic rise in the demand for digital financial services. We are seeing many new, more efficient financial solutions, such as online deposits, mobile wallets, electronic bill payments, etc.

Unsurprisingly, these are gaining mainstream acceptance via the proliferating Fintechs and neo-banks, as they simplify and streamline the customer’s total banking experience.

This article offers a quick roundup of why the banking industry will continue to make upbeat digital and technology investments.

The world is flat

Today, geography is fast becoming history.

The revolutionary changes that Internet has powered in the last two decades have made a sea change to the way everything operates – people, profits, and the planet. Each day innovative spending models can be seen over E-commerce and the ways to pay for them (wallet tech and buy now pay later models etc.).

Be it opening bank accounts virtually with e-KYC, transacting cheques, balancing accounts, clearing utility bills, or setting up payment instructions. There is little that cannot be done online today.

Expect customer dependence to rise on digital banking (especially with the onset of 5G, IoT, and Voice Banking Tech). All roads, it appears, lead to banking technology.

High Accuracy Banking

Human precision and expertise – still essential to the banking industry – have been increasingly replaced with intelligent machines. The error rates have decreased manifold as the productivity rates in banking operations have soared exponentially.

Also, the way data and information can be safeguarded in the new digital order is of a different magnitude – far more foolproof.

New mandates are introduced regularly to elevate the customer experience. Take, for instance, ISO 20022. A rich, structured, and extensible messaging standard that creates a common language and model for payment data across the globe. By 2025, when the high-value payment systems are migrated and harmonized, the global banking ecosystem will be elevated to a new reliable and resilient value transfer platform – expect even higher accuracy and customer-centricity.

Quality of Living

In its unusual ways, the pandemic has made people aware of the quality of their lives – the importance of work, family, relationships, and other existential matters surfaced like never before. The era of resignations in the western world followed as substantial numbers prioritized meaning over money.

As digital adoption and smartphone usage grew en masse, every aspect of the business was transformed. There was simply no way that the traditional banking process – tedious and time-consuming as they were – would find space in the new emerging paradigm.

In the internet and mobile banking world, frictionless, omnichannel, and hyper-personalized customer journeys are more than buzzwords.

As one considers how most banking disruptors – led by Neobanks and Fintechs and the subsidiaries of the tech giants – are creating loyal customers amongst the millennial and digital natives demographic, the writing is evident on the wall – only companies mastering the art of technology that deliver unprecedented customer value will thrive.

Power of Tech Intelligence to Boost Top and Bottom lines.

A direct impact on banking revenues and profits can be gleaned from the Reserve Bank of India’s (RBI) call to all Indian banks to implement Business Intelligence (BI)as part of their retail, corporate, and wealth management operations.

A BI system highlights the past through analyses and simulates the future by extrapolating current trends. With this information, FIs cannot only make prescient judgments on markets and money management but also boost productivity, efficiency, and, ultimately, profits.

Conclusion

As the year progresses, customers’ reliance on digital banking services will increase. Banks still have enormous room to grow. More customer loyalty can be earned by investing in cutting-edge tech to modernize their operations, streamline processes, and increase flexibility.

As Open Banking, Blockchain, Wearables, Biometrics, Chatbots, and Voice tech see increasing adoption across Financial institutions; more legacy organizations will seek collaborative approaches to learn and work with fintech companies and neo-banks.